What Fees Do Sellers Pay

When Selling a Home

in Murrieta?

Selling your home is exciting — but the closing costs can catch you off guard if you do not know what to expect. Here is a complete breakdown of every fee and cost you will likely encounter, with real numbers based on Murrieta and Riverside County.

Why Understanding Seller Fees Matters

One of the most common questions we hear from sellers is: "What am I actually going to walk away with?" It is a fair question — and one that too many agents gloss over until you are deep into the process. We believe you should understand every cost before you ever list your home. That transparency is what helps our clients make confident, informed decisions rather than feeling blindsided at closing.

In Murrieta and across Riverside County, the fees you will encounter as a seller are fairly predictable. Some are standard across every California transaction. Others depend on your specific property — whether you are in an HOA, whether you have Mello-Roos, or whether you have existing liens. This guide covers all of it, so you know exactly what to budget for.

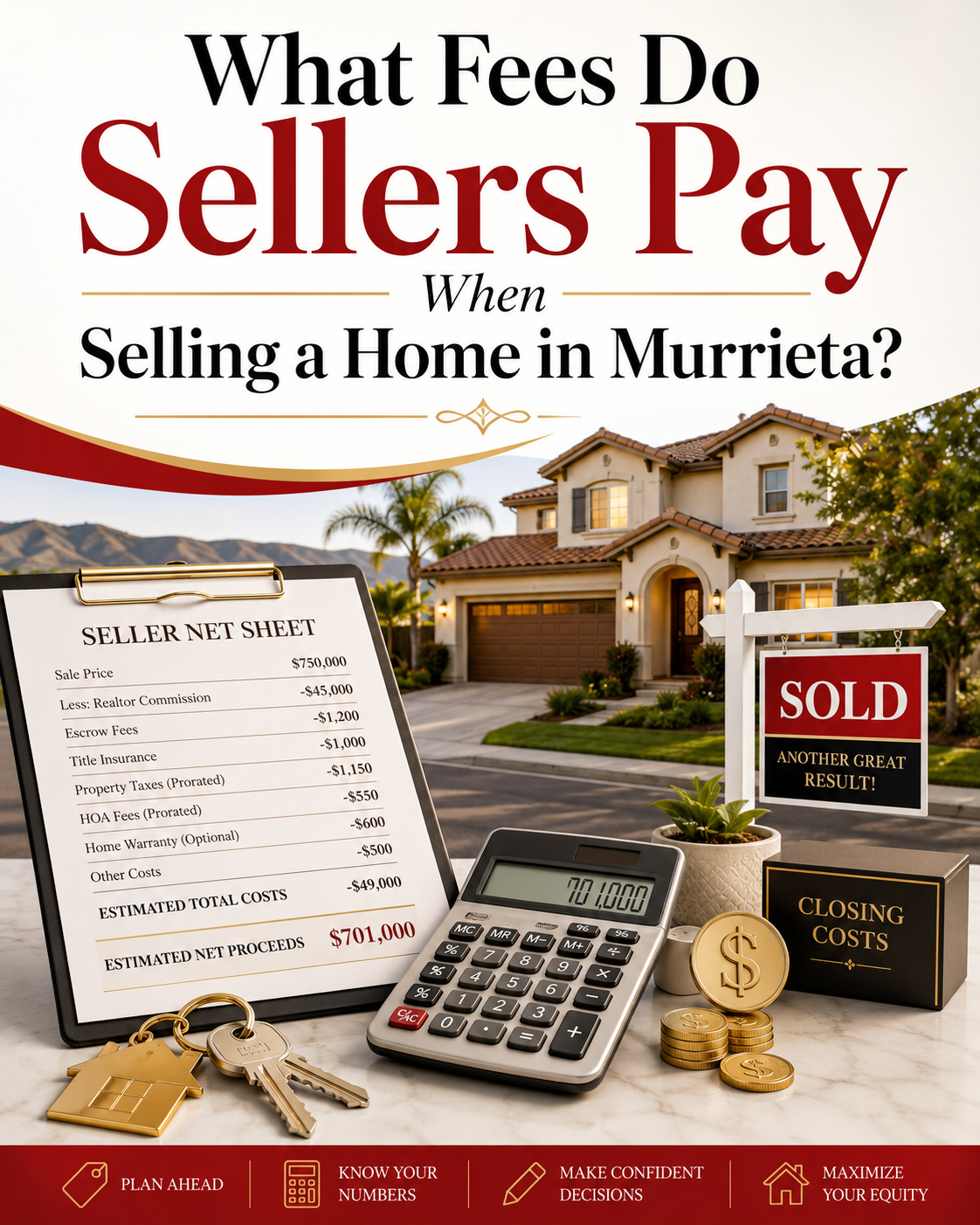

Below, you will find a detailed explanation of each fee, what it covers, and who typically pays for it. At the end, we include a real-dollar example showing what a Murrieta seller might pay on a $600,000 home and a $900,000 home. As your Realtors® and listing agents, we prepare a comprehensive Seller Net Sheet that clearly outlines your estimated selling expenses and projected net proceeds, giving you a precise financial picture of the sale.

In This Guide

Complete Breakdown of Seller Fees

Every fee is explained in plain language — no surprises, no confusion. Click each section to learn exactly what you are paying for and why.

Real Estate Agent Commissions

Negotiated — based on services & scope

The largest selling cost, now separately negotiated for the listing agent and — if offered — the buyer's agent.

Read the full explanation

Following recent industry changes, real estate commissions are no longer structured around a single fixed percentage. Instead, there are two separate and independently negotiated compensation agreements — one for the listing agent and one for the buyer's agent.

**Listing Agent Commission:** The compensation you pay your listing agent is negotiated directly between you and that agent. There is no standard fixed rate. The commission is based on the scope of services provided, your home's marketing strategy, the level of representation required, and the complexity of the transaction. A listing agreement spells out exactly what your agent will do — from pricing and preparation to marketing, negotiation, and closing — and what that service is worth. This is something we discuss in detail during our listing consultation so you have full clarity before signing anything.

**Buyer Agent Compensation:** Sellers may also choose whether to offer compensation to a buyer's agent. Your listing agent can make recommendations on what you might offer to compensate a buyer\'s agent, but the actual buyer agent compensation is negotiated as part of the purchase offer. The buyer and their agent submit an offer that may include a request for the seller to compensate the buyer\'s agent, and you can accept, reject, or counter that term just like any other part of the offer. This gives you full flexibility and control over the final agreement. Compensation can be structured in a variety of ways — as a flat amount, a percentage, or through other negotiated terms — and the details are always outlined in writing.

What this means for you as a seller: you have more transparency and more control than ever before over how and what you pay for real estate representation. We walk you through every option, explain the implications of each approach, and help you structure the compensation in a way that is fair, competitive, and aligned with your goals.

What you are paying for: professional pricing strategy, marketing, photography, negotiation, contract management, and guidance through every step from listing to closing. A strong listing agent protects your interests, manages the timeline, and can often help you net more than you would on your own — even after commissions.

On a $600,000 Home

Varies — negotiated with agent

On a $900,000 Home

Varies — negotiated with agent

Are You Saving on Fees—or Losing on the Sale?

Choosing a discount brokerage may reduce the commission shown on paper, but the fee is only one part of your final outcome. Limited marketing, weaker pricing strategy, reduced availability, fewer showing opportunities, and less experienced negotiation can affect how quickly your home sells, the strength of the offers you receive, and the amount you ultimately keep.

It is also worth considering this: if an agent is quick to reduce their own compensation at the first request, how confidently will they defend your price and negotiate your equity when a buyer asks for concessions?

A skilled, accredited broker brings more than a listing agreement. Strategic preparation, professional presentation, broad market exposure, careful offer evaluation, and strong negotiation can protect your equity throughout the transaction. Saving on the front end may seem appealing, but sellers can ultimately walk away with less if the home is underexposed, poorly positioned, or not negotiated effectively.

The goal should not simply be to pay the lowest fee. It should be to achieve the strongest possible net proceeds, with experienced representation guiding the sale from pricing through closing.

Owner's Title Insurance Policy

~$1,800 – $2,500 (varies by sale price)

In Riverside County, the seller traditionally pays for the owner's title insurance policy, which protects the buyer against title defects.

Read the full explanation

Title insurance protects the buyer (and their lender) against any claims, liens, or defects on the title that existed before the sale. In Riverside County, it is customary — though not legally required — for the seller to pay for the owner's title insurance policy. The lender's title policy is typically paid by the buyer.

The cost of an owner's title policy varies based on the sale price, but for homes in the $600,000 to $900,000 range, you can generally expect somewhere between $1,800 and $2,500. This is a one-time premium paid at closing.

Title insurance is one of those costs that buyers rarely think about — but it is an important part of a clean closing. We coordinate with the title company to make sure everything is handled properly and that you understand what you are paying for.

On a $600,000 Home

~$1,800 – $2,000

On a $900,000 Home

~$2,200 – $2,500

Riverside County Documentary Transfer Tax

$1.10 per $1,000 of sale price

Riverside County charges a documentary transfer tax of $0.55 per $500 of the sale price (equivalent to $1.10 per $1,000).

Read the full explanation

The documentary transfer tax is a county-level fee charged when real property changes hands. In Riverside County, the rate is $0.55 per $500 of the sale price, which works out to $1.10 per $1,000 of value.

This tax is customarily paid by the seller in Riverside County. It is collected at closing through the escrow company and remitted to the county recorder when the deed is recorded.

The City of Murrieta does not impose an additional city-level documentary transfer tax on top of the county rate. So for a property within Murrieta city limits, the total transfer tax is simply the Riverside County rate.

This is one of the smaller costs sellers pay, but it is important to include it when calculating your expected net proceeds.

On a $600,000 Home

~$770

On a $900,000 Home

~$1,155

HOA Document Fees & Transfer Fees

$500 – $1,500+ (varies by HOA)

If your home is in an HOA community, expect to pay for document preparation, transfer fees, and sometimes capital contribution fees.

Read the full explanation

Many Murrieta communities have homeowners associations — Spencer's Crossing, Greer Ranch, Mahogany Hills, and others. If your property is in an HOA, there are several fees that typically come up during the selling process.

Common HOA-related costs include:

• HOA Document Package (Transfer Disclosure Statement, CC&Rs, bylaws, financials, etc.) — typically $200–$500

• HOA Transfer Fee — typically $200–$400, charged when the membership is transferred to the new owner

• Capital Contribution or Working Capital Fee — some HOAs charge a one-time fee of $200–$1,000+ when a unit is sold

• Demand for Payment / Status Letter — typically $50–$100

The exact fees depend on your specific HOA. We will review your CC&Rs and fee schedule as part of our listing preparation so you know exactly what to expect. If you are not sure whether your property is in an HOA, we can help you figure that out — it is one of the first things we look at.

On a $600,000 Home

~$500 – $1,000

On a $900,000 Home

~$500 – $1,500

Prorated Property Taxes

~1.1%–1.25% annually (prorated at closing)

You are responsible for property taxes up through the day of closing. In Murrieta, the base tax rate is roughly 1.1%–1.25% of assessed value, plus Mello-Roos in some areas.

Read the full explanation

Property taxes in California are paid in arrears, meaning the bill you receive covers a period that may extend beyond your ownership. At closing, your share of property taxes is prorated — you pay only for the portion of the year you owned the home, and the buyer picks up the rest.

In Murrieta, the base property tax rate is approximately 1.1% to 1.25% of the assessed value, though the actual amount can vary depending on the property's purchase history under Proposition 13. Some newer communities also have Mello-Roos (Community Facilities District) assessments, which add an additional annual fee that is also prorated at closing.

For a home assessed at $700,000 with a typical rate of 1.15%, the annual property tax is roughly $8,050. The prorated amount you pay depends on when in the tax cycle the sale closes. We make sure the escrow company calculates this correctly — it is a standard part of every transaction.

On a $600,000 Home

~$2,000 – $4,000 (prorated)

On a $900,000 Home

~$3,000 – $5,000 (prorated)

Natural Hazard Disclosure Report

$200 – $400

A standard required disclosure in California, typically costing $200–$400, informing the buyer of natural hazard zones and environmental conditions.

Read the full explanation

California law requires sellers to provide buyers with a Natural Hazard Disclosure (NHD) report. This report identifies whether the property falls within any state-mandated natural hazard zones — earthquake fault zones, flood zones, wildfire hazard areas, seismic hazard zones, and more.

The NHD report is typically prepared by a third-party disclosure company and costs between $200 and $400. In most cases, the seller pays for this report. It is ordered early in the listing process and delivered to the buyer as part of the disclosure package.

Some parts of Murrieta and the surrounding area may fall within wildfire hazard zones or other designated areas, so this disclosure is particularly important for properties on hillside or rural lots. We order this report as soon as a property is listed to keep the transaction timeline on track.

On a $600,000 Home

~$300

On a $900,000 Home

~$300

Preliminary Change of Ownership Report (PCOR)

Included in escrow fees (minimal direct cost)

A form filed with the county assessor that documents the change of ownership for property tax reassessment purposes.

Read the full explanation

When a property is sold in California, the assessor needs to determine whether the property will be reassessed for property tax purposes under Proposition 13. The Preliminary Change of Ownership Report (PCOR) is the form that documents the details of the transaction.

The PCOR is filed with the Riverside County Assessor's Office, and it is typically prepared by the escrow company as part of the closing process. There is generally no filing fee charged to the seller for this form, though the escrow company may include its preparation as part of the escrow service.

This is one of those behind-the-scenes items that sellers rarely think about, but it is an important part of the California property tax system. We make sure it gets handled correctly so there are no issues after closing.

On a $600,000 Home

Included in escrow

On a $900,000 Home

Included in escrow

Home Warranty (Optional but Common)

$600 – $900

Sellers often offer a home warranty to buyers as an incentive, typically costing $600 to $900 for a one-year plan.

Read the full explanation

A home warranty is an optional service contract that covers the repair or replacement of major home systems and appliances for one year after closing. While it is not required, many sellers choose to offer a home warranty as a selling point — it gives buyers peace of mind and can help reduce the risk of post-closing repair disputes.

For a standard single-family home in the Murrieta area, a one-year home warranty plan typically costs between $600 and $900. The seller pays this premium at closing. Coverage usually includes the HVAC system, plumbing, electrical, water heater, oven/range, dishwasher, and more.

In our experience, offering a home warranty is a smart move. It shows good faith to the buyer and can make your listing more attractive, especially if your home has older systems. We can help you select a reputable home warranty provider and choose the right coverage level.

On a $600,000 Home

$600 – $900

On a $900,000 Home

$600 – $900

Escrow Fees

~$1,000 – $1,500 (seller's portion)

The escrow company charges a fee for handling the transaction. In Riverside County, escrow fees are typically split between buyer and seller or negotiated.

Read the full explanation

The escrow company acts as a neutral third party that manages the exchange of funds and documents between the buyer and seller. They handle the money, ensure all conditions of the sale are met, and coordinate the final recording of the deed.

Escrow fees in Riverside County are typically split between the buyer and seller, though this is always negotiable as part of the purchase agreement. The total escrow fee is usually around 1%–2% of the sale price (combined for both parties).

For a $700,000 home, total escrow fees might be in the range of $2,000–$3,000, with the seller's share typically being around $1,000–$1,500. The exact fee depends on the escrow company and what was negotiated in the contract.

We work with experienced local escrow officers who are responsive and detail-oriented. A good escrow officer is worth their weight in gold when it comes to keeping a transaction on track.

On a $600,000 Home

~$1,200

On a $900,000 Home

~$1,500

Recording Fees

$75 – $200

The county charges a small fee to record the deed and other documents. Typically a nominal amount paid by the seller.

Read the full explanation

When the sale closes, the new deed and any other documents (such as a deed of trust or release of lien) need to be officially recorded with the Riverside County Recorder's Office. This creates a public record of the ownership transfer.

Recording fees are relatively small — typically ranging from $75 to $200 depending on the number of pages being recorded. In most transactions, the seller pays for the recording of the grant deed, while the buyer pays for recording their new deed of trust with the lender.

This is one of the smallest costs in the transaction, but it is a necessary step to complete the transfer of ownership.

On a $600,000 Home

~$100

On a $900,000 Home

~$125

Outstanding Liens or Judgments

Varies (mortgage payoff is standard)

Any existing liens (mortgage payoff, HELOC, mechanic's liens, tax liens) must be satisfied before or at closing.

Read the full explanation

Before a property can be sold with a clean title, any outstanding liens or judgments against the property must be paid off. The most common lien is your existing mortgage, which is paid from the sale proceeds at closing through the escrow process.

Other types of liens that may appear include:

• Home Equity Line of Credit (HELOC) or second mortgage

• Mechanic's liens (from unpaid contractor work)

• Tax liens (from unpaid property taxes or IRS liens)

• Judgment liens from court orders

All of these are handled through escrow — the title company runs a title search before closing and identifies any liens that need to be satisfied. Your mortgage payoff is not an "extra" cost; it is simply the balance you already owe being paid off from the sale proceeds. But it is important to understand that the net proceeds you walk away with are the sale price minus all of these costs and obligations.

We review your property's title status early in the listing process so there are no surprises during escrow.

On a $600,000 Home

Depends on existing mortgage

On a $900,000 Home

Depends on existing mortgage

Buyer Credits (Repairs or Closing Cost Assistance)

Varies (negotiated)

In negotiations, sellers sometimes agree to credit the buyer for repairs, closing costs, or other concessions.

Read the full explanation

During the negotiation process, a buyer may request that the seller provide a credit toward repairs identified during the inspection, or toward their closing costs. This is entirely negotiable — there is no requirement for a seller to agree to any credits.

Common scenarios include:

• Repair credits: The buyer requests a credit to handle repairs after the inspection (e.g., a roof repair, HVAC service, or plumbing issue). This is often simpler and faster than arranging the repairs yourself.

• Closing cost credits: In some market conditions, sellers may agree to contribute toward the buyer's closing costs to help keep the deal together or make the offer more competitive.

The amount of any credits is always negotiated. In a seller's market, credits are less common. In a buyer's market or when inspection issues arise, credits become a normal part of getting to closing.

We help you evaluate every credit request carefully and negotiate from a position of strength — making sure you give up as little as possible while still keeping the transaction on track.

On a $600,000 Home

$0 – $5,000 (if negotiated)

On a $900,000 Home

$0 – $5,000 (if negotiated)

Murrieta Seller Fee Estimate Examples

Here is what your total selling costs might look like on two common Murrieta price points. These are estimates — your actual costs will depend on your specific property, HOA, existing mortgage, and negotiated terms.

Example: $600,000 Home

Example: $900,000 Home

Important: These estimates do not include your existing mortgage payoff, which is typically the largest amount deducted from your sale proceeds. Your actual net proceeds will be the sale price minus all selling costs minus your mortgage payoff. We provide a personalized net sheet for every client that includes your exact mortgage balance.

Key Takeaways for Murrieta Sellers

Budget 7–9% for Selling Costs

When you factor in commissions, closing costs, and a reasonable allowance for repairs or credits, plan on roughly 7% to 9% of your sale price going toward selling expenses. On a $700,000 home, that is about $49,000 to $63,000.

Commissions Are Negotiable

There is no law or rule that sets a specific commission rate. It is always negotiable between you and your agent. What matters is the value you receive — strong marketing, expert negotiation, and smooth execution can more than pay for themselves.

HOA Fees Can Add Up

If you are in an HOA community, the document fees, transfer fees, and potential capital contribution fees can add $500 to $1,500 or more to your selling costs. We review your HOA documents early so these are never a surprise.

A Net Sheet Is Your Best Friend

Before you list, ask your agent for a seller net sheet that estimates your actual take-home after all costs. We prepare a personalized net sheet for every client during our listing consultation — it is the best way to plan your next move with confidence.

Frequently Asked Questions About Seller Fees

What is the biggest cost when selling a home in Murrieta?

The biggest single cost is the real estate agent commission, which typically totals 5–6% of the sale price. On a $700,000 home, that is roughly $35,000 to $42,000. This is negotiable and varies depending on the services provided. Everything else — title, escrow, taxes, disclosures — adds up to a smaller portion of your total selling costs.

Do sellers always pay for title insurance in Riverside County?

It is customary in Riverside County for the seller to pay for the owner's title insurance policy, but it is not a legal requirement. The allocation of title insurance costs is negotiable as part of the purchase agreement. In practice, most sellers in our area do pay for the owner's policy.

How much are closing costs for sellers in California?

Beyond commissions, typical seller closing costs in California range from roughly 1% to 3% of the sale price. This includes title insurance, escrow fees, transfer taxes, HOA fees, prorated property taxes, and disclosures. On a $700,000 home, you might expect $7,000 to $21,000 in non-commission closing costs.

What happens if my home is not in an HOA?

If your property is not in a homeowners association, you simply will not have HOA-related fees. Many older neighborhoods in Murrieta are not HOA communities, while newer master-planned communities typically are. We confirm your HOA status and review any associated fees during our initial listing consultation.

Should I offer a home warranty to the buyer?

It is optional, but offering a home warranty is a smart strategy in most cases. It costs you $600 to $900, but it gives buyers confidence, reduces the likelihood of post-closing repair disputes, and makes your listing more competitive. We recommend it in most situations, and we can help you select the right plan.

What is Mello-Roos and will I have to pay it?

Mello-Roos is a special tax district assessment that applies to some newer communities in Murrieta. If your property is in a Mello-Roos district, that annual assessment is prorated at closing — you pay for the days you owned the home, and the buyer takes over for the rest of the year. Not all properties have Mello-Roos, and we will let you know if yours does.

What does a net sheet show me?

A seller net sheet is an estimate that shows your expected sale price minus all selling costs and existing obligations (like your mortgage payoff). It gives you a clear picture of what you will actually walk away with at closing. We provide a personalized net sheet for every client — it is one of the most important tools for making a confident decision about listing your home.

Want to Know Exactly What You Will Walk Away With?

This page gives a general overview of the fees and costs sellers can expect when closing a home in Murrieta, but every situation is different. That is why one of the first steps we take once you are under contract is preparing a detailed seller net sheet — included as part of your seller package. It gives you an accurate estimate of exactly what you will walk away with after all fees and costs, breaking down every line item — commissions, title, escrow, transfer tax, HOA fees, prorated taxes, your mortgage payoff, and more — all specific to your property and sale price so there are no surprises at closing.